| High | Low | High | Low | |||

| EUR/USD | 1.0931 | 1.0907 | USD/ZAR | 12.7433 | 12.7012 | |

| GBP/USD | 1.5525 | 1.5493 | GBP/ZAR | 19.77 | 19.69 | |

| EUR/GBP | 0.7052 | 0.7030 | USD/RUB | 66.44 | 63.15 | |

| USD/JPY | 124.86 | 124.66 | USD/ILS | 3.8086 | 3.7861 | |

| GBP/CHF | 1.5244 | 1.5200 | S&P 500 | 2,088 | 2,081 | |

| GBP/AUD | 2.1134 | 2.0998 | Oil (Brent) | 50.34 | 49.94 | |

So we had the first Bank of England ‘super Thursday’ yesterday. This new invention where the central bank publishes its inflation report and monetary policy minutes at the same time as the latest rate setting decision. The pound sterling didn’t like it, it fell 0.75%! What did for GBP was the fact that economists were expecting 2 of the 9 voters to push for an interest rate hike, but only one did. This implies that the committee is somewhat less hawkish than the market anticipated. Never a good thing for a currency. In particular the chances of a rate hike in 2015 have diminished considerably. That’s not to say that Governor Carney is not bullish on the UK economy, in fact he raised his estimation of UK growth this year and he is more optimistic about productivity and wage growth than before. All in all a more balanced picture for the UK economy emerged, which is all to the good, although the pace of employment growth could definitely be better.

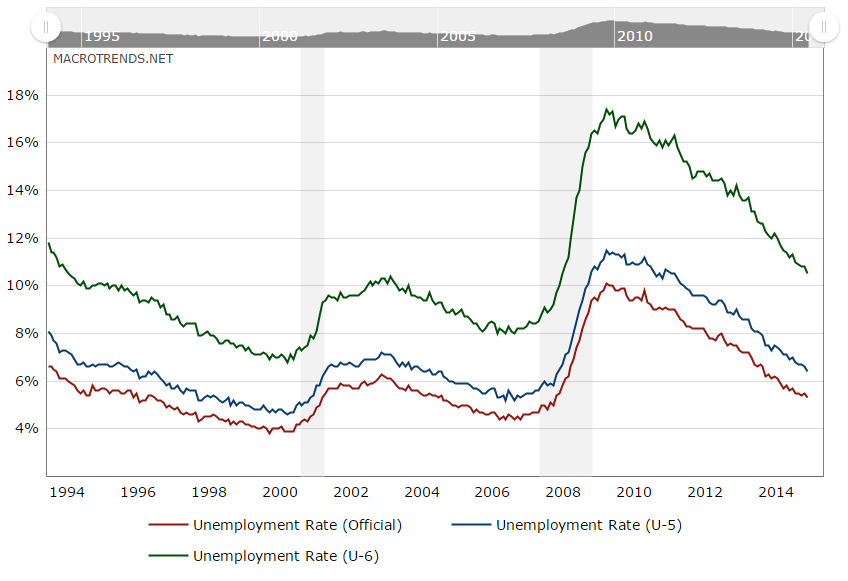

It’s a big day for macro today with the U.S employment report published in the early European afternoon. Before I go into it, I should tell you that economists expect the Federal Reserve to implement their first interest rate hike in September. Today experts are forecasting a 223,000 addition to payrolls and the unemployment rate remaining steady at 5.3%. They also expect a 0.2% rise in average hourly earnings. In the last FOMC minutes,policy makers remarked that “some further improvement in the labour market” was desirable before the process of normalisation would commence. It should be noted that the Federal Reserve’s estimation for full employment is an unemployment rate at 5 – 5.2% in along with further signs of a tightening labour market. But the current data is contradicted by alternative measures of employment trends which capture part-time workers and discouraged workers. On this basis the unemployment rate is yet to recover to the levels that existed before the global financial crisis in 2008 (see chart below). The one really encouraging thing in the chart is that the trend is clear and continuing to improve. Wage growth remains anaemic considering the level of the unemployment rate, although perhaps it’s more understandable if you believe the alternative measures are a better representation of labour conditions or indeed if you consider importance of the participation rate which hovers at levels not seen since the dark days of incomes policies and stagnation in the 1970s. Bottom line, if we get better data than the market expects it will reinforce the conviction that we will see the Federal Funds rate rise for the first time since 2006. This could be the day that breaks the back of EUR/USD and GBP/USD’s stubborn buoyancy. More on that in a bit…

{Source:- http://www.macrotrends.net/1377/u6-unemployment-rate}

Before I focus more on our near term views on the major currencies I’ll spend a bit of time on Nigeria, and the naira. Nigerians and international observers have raised concerns about the time it’s taking for the new President to put together his team. As of now there is still no insight into who will take up the main ministerial portfolios. I confess I too have shaken my head in frustration at these events, but as we all know, ignorance invites sloppy thinking. There is method to this, and a deeper understanding of the new incumbent’s main objectives is essential to add a context to the seeming limbo. It seems that the new President is very serious about combating corruption, and we should applaud him for this. All candidates for ministerial posts are being vetted, as they should. So far some of his initial picks may not have been able to stand up to the scrutiny. This President is prepared to wait until the right people, capable and honest people are vetted. It is expected that the process will not be complete for another month, but surely this is worth waiting for? Meanwhile the naira has been on quite a journey in recent weeks. Concerns about the lack of policy direction had put the naira under pressure, but a few days ago commercial banks were urged to stop accepting foreign currency cash deposits in a move expected to reduce speculation. Coupled with news that President Buhari plans to reduce recurrent expenditure in next year’s budget and focus more on development projects, the naira was able to gain about 4%. Of course the central bank selling $80m of foreign currency didn’t hurt. The central bank will continue to resist calls to allow the currency to devalue, despite the continued weakening in Nigeria’s main export… oil. In case you missed it, the black gold is flirting with sub $50 levels again and the Iranian deal isn’t going to add a bid to it any time soon! There seems to be an air of realism about this new Nigerian administration, but until the ministerial positions are filled it is too early to pass judgement. The President seems very serious about getting the giant of Africa on the right path, let’s hope macro events are kind to him.

Back to the majors… I have watched over the last few days as first EUR/USD flirted with the July lows but didn’t quite make it down to 1.0808, and then GBP/USD in the wake of the Bank of England’s super Thursday announcement yesterday fell sharply and tested but did not breach an interim low at 1.5467 (the more significant level to watch remains 1.5330). These currency pairs continue to hold on and avoid what we all expect… dollar appreciation. As I mentioned in a recent blog, the longer it takes for this to happen, the more impressive the build-up of potential energy becomes, the more significant the fall is likely to be. I am of the belief that GBP/USD is likely to be weaker than EUR/USD. In fact I grow more and more sceptical about when we are likely to see EUR/USD parity. Don’t get me wrong, I expect it to happen, I just think it might take considerably longer to happen than I originally expected. For those of a technical nature, here’s an illustration of what I’m thinking…

This is long term though. For those with more immediate needs, we don’t expect too much excitement before the big data this afternoon. Data meeting expectations or surpassing it can only boost the dollar at this point…

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc