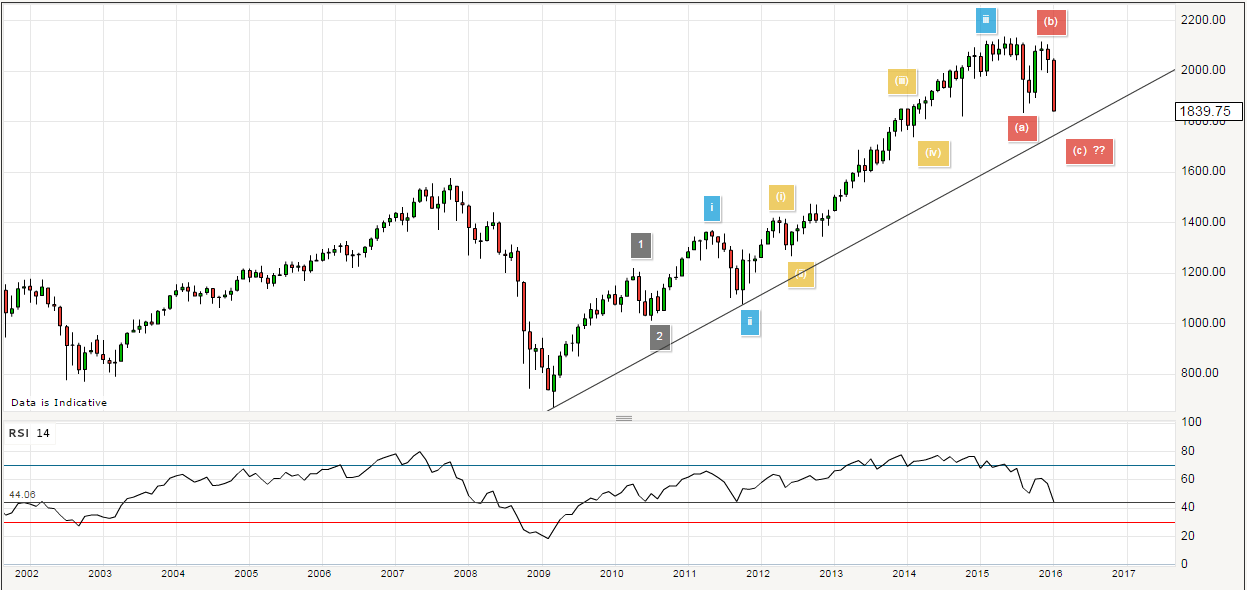

The list of equity indices entering bear market territory grows with Nigeria and more importantly Japan some of the latest entrants – the official definition of a bear market is generally taken to mean a greater than 20% decline in an index. The culprit, at least according to the papers seems to be investor concerns about falling oil prices. If that’s the reason for this decline, then this represents a fantastic opportunity to buy consumer stocks which will benefit from the higher disposable incomes consumers will have due to lower energy bills. There’s a silver lining in all things if you only look hard enough. Fundamentals aren’t my strength, but when I look at the charts this seems like an inevitable correction within the context of the great bull market we have seen since the lows of March 2009.

As you can see from the chart above we are approaching a bigger picture trend line and we remain well within the bounds of a longer term bullish trend. But obviously that’s just my take on it.

According to the Financial Times yesterday, leading economists at the World Economic Forum in Davos are concerned about the state of the global economy at the moment. The confluence of (i) falling commodity prices, (ii) decelerating growth in China and (iii) excessive dollar denominated debt in developing countries means that another leg of the global financial crisis could occur. It’s a definite possibility, but let’s not kid ourselves all three of those situations are pretty much tied together. Slowing growth in China is largely responsible for declining commodities prices and Chinese corporates are as guilty as anyone for over leveraging in dollar debt. Even so, it doesn’t make the risk less valid, and it does mean that Chinese authorities will need to tread carefully as there’s only so much they can allow the renminbi to weaken. Too much and they could exacerbate the pressure of dollar debt on Chinese companies. You’ll recall, I hope, that I have been writing about the indebtedness of emerging market corporates as a potential problem over the last half year.

It appears the governor of the Bank of England shares the pessimism of the Davos economists because he has buried any chance of rate rises in the UK any time soon. In the middle of last year, when the UK was basking in the sunshine of a Tory election victory, unemployment was falling and Britain was near the top of the list for developed economy growth statistics he observed that early 2016 would likely be a time when the MPC would have to seriously consider initiating a process of rate normalisation. Well… here we are in early 2016 and his economic outlook is definitely chillier and it’s not because of the sub-zero temperatures we’re suffering here in South Eastern England. Wage growth, like in the United States, has failed to pick up in the UK; the current account is in deficit and doesn’t look healthy at all; and then we have the bad news in China and negative risk sentiment globally. It’s not difficult to understand Mr Carney’s reasoning. The pound sterling continues to plumb new multi-year lows and as I mentioned recently sub-1.40 GBP/USD looks a near certainty now. Sometimes you can devalue and not even look like you’re doing it. I bet Mario Draghi is jealous right now!

I continue to believe that emerging market currencies will remain under pressure as weaker commodities prices will inevitably translate into tougher policy choices for governments and discoveries that emerging market corporates have over extended themselves. It’s just a matter of time. I will however note that the euro has remained fairly stable against the dollar while the Japanese yen has unquestionably been strengthening in recent weeks. The pound is doing its own special thing and there’s no reason for that to stop any time soon. It seems likely that current trends will persist at least until equity markets find their support levels. For my part I’m not ready to see this as a crisis, but if I see the S&P spend a decent amount of time through my bigger picture trend-lines then I’m ready to be persuaded. By the way that would require more than a 5% fall from here, it’s not that far away but somehow I struggle to be concerned right now. January’s always seems to give us this type of excitement before calmer heads prevail…

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc