This evening the Chairwoman of the Federal Reserve, Janet Yellen, will make her semi-annual speech to Congress in which she will give her outlook for the US economy and discuss monetary policy. As I’ve mentioned in recent blogs, the greenback has been largely under pressure versus its peers since the start of the year (the euro is up 4% versus the dollar in 2016) as the market has reassessed the likelihood of further rate hikes in 2016. Increasingly the tough global economic climate and turbulent conditions for stock market’s sees investors more and more confident that the Federal Reserve will be unable to make further progress in its normalisation strategy, indeed many now think the US central bank erred by raising interest rates in the first place, and you can see this in the price action in the money markets. It is likely that Chairwoman Yellen will try to maintain the stance that the Federal Reserve took in December but with a more cautious tone about the outlook for the global economy and the likely impact on the US economy. Many top bank strategists are already looking at this testimony as a seminal moment for 2016. One thing is clear, if Yellen backtracks we could see a further large selloff in the dollar, I just find it hard to believe that institutional inertia will permit the Federal Reserve to give up so quickly.

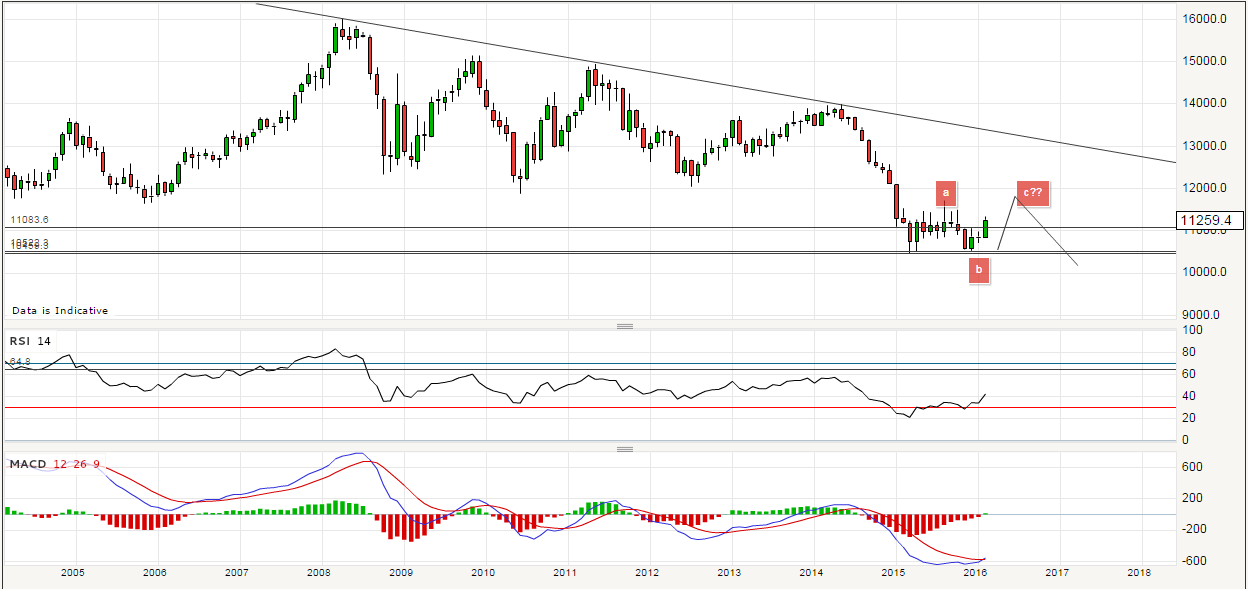

There are a number of things that could change my view, we are seeing signs of systemic risk within the energy sector for example, as beleaguered corporates are under pressure coping with their outstanding debts while facing collapsing revenue, there are also worries about the contingent convertible bond market in Europe which affects European banks. Either or both of these issues could cause severe problems that could spill over into the wider economy and tip the scales back towards another Global Financial Crisis style panic. And don’t get me started about the mountains of dollar debt issued by Emerging Market corporates and the problems they’re likely to face as their home currencies depreciate. There is a lot to worry about, but I’m not a market fundamentalist, my focus will always remain squarely on the technical factors underlying the key charts that I monitor, and on that basis I am not yet ready to capitulate from my view that the longer term bull market that started in March 2009 is intact. We would need to see a lot more damaging price action for my view to change (perhaps another 25% decline in the S&P 500 would do it). In addition, from a bigger picture technical perspective, the bounce in EUR/USD is far from unexpected and it looks to me to be the final corrective wave up before the bearish trend (stronger dollar) reasserts itself. The only issue is that the corrective wave could easily take EUR/USD up to even the low 1.20s before running out of steam. At the moment the weaker dollar seems synonymous with negative risk sentiment so the implication is quite clear, and the fact that this could persist for weeks or even possibly months means that this could be an ugly and uncertain first quarter of 2016.

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc