We’ve got some encouraging data from the two largest economies in the world, the United States and China. Yesterday’s non-manufacturing ISM data in the United States showed a services sector which if anything strengthened slightly more than expected, when you consider that this is by far the largest component of US gross domestic product it is heartening news indeed. And in China the Caixin Services PMI also showed stronger than expected improvement, which might optimistically be taken as evidence that the economy of the Middle Kingdom is stabilising. Most analysts believe this is a consequence of the stimulus efforts implemented by the Chinese government already, but there are risks inherent in this, as the most likely sectors to benefit – property and finance – are to a large extent areas where substantial reform will be needed for the longer term health of the Chinese economy. It’s also worth pointing out that Eurozone retail sales came out much stronger than expected yesterday growing 2.4% year on year to February, and the services PMI in the UK was also stronger. Perhaps the real theme is the strength of the non-manufacturing sector in the major economies.

Whether the good news is a real turning point or not, markets seem to be reacting positively today, the dollar is stronger, equities are up and oil has been on a tear this morning, already up 2%. Of course regarding oil, this could also be because of news about falling rig counts in the US, and signs that OPEC might be able to come up with some sort of output freeze (I’ll believe that when I see it!). With regards to currencies, it will take more than what we’ve seen today to convince me that the counter-trend rally (dollar weakening) is over. The pound sterling and Japanese yen offer a bit more clarity than most of the other major currencies, the former is chronically weak, and the other is the best performing liquid currency so far this year. The strength of the Japanese yen is now of such concern that we are starting to hear comments from Prime Minister Abe, unfortunately this isn’t having much of an impact yet, this might have to run its course.

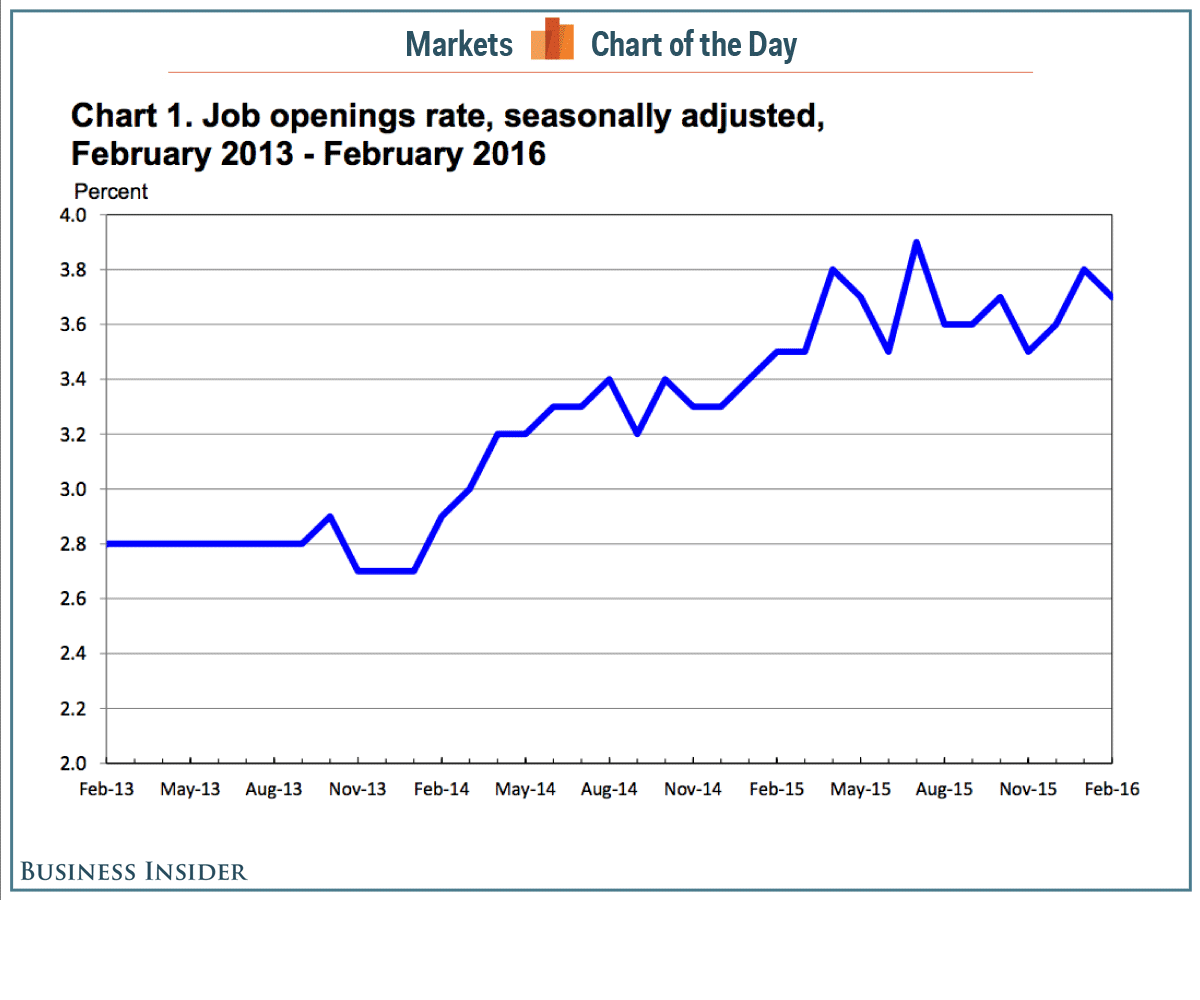

Finally, below is chart for job openings in the United States, which is collated from the JOLTS survey. It’s possible job opportunities in the US have peaked. Something to monitor in coming months as this could have a substantial impact on the US hiking cycle. Here is the Business Insider article that discusses the chart below…

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc