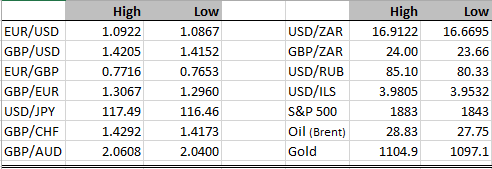

I think it was Warren Buffet who said “be fearful when others are greedy, and greedy when others are fearful”. In retrospect yesterday seemed like a good day for greed. That’s not to say I’m calling a bottom on the recent market turbulence, but it does illustrate the wisdom of Mr Buffet’s mantra. As I pointed out yesterday, this feels like a correction within the context of a longer term equity market bull trend. At the end of the day, what’s the latest thing to hammer the oil price? The Iranians are back in the market, a potentially huge economy that has been shunned for a decade will be able to participate fully in the global economy, I’m not sure that’s a bad thing at all. Falling energy prices will be harmful for the energy sector and there will of course be derivative spill overs (lost jobs in sectors that benefit from the energy sector etc.), but surely this will not match the positives from consumers with deeper pockets? That’s not to say that there aren’t concerns regarding the global economy, there are. In particular China. But consider this, the US economy is chugging along reasonably well, Europe is slowly recovering, consumers everywhere are about to get a massive boost to their income from lower energy costs, and does anyone really believe the Chinese aren’t going to work to counter the slowdown? So yes things look grim, and there are a host of negatives that one could reel off, but it just doesn’t feel like disaster yet to me.

The front page of the Financial Times (at least the online edition anyway!), talks about ECB resistance to further stimulus at the moment. The European central bank would at least like to wait until the spring to make a decision about the impact of the current volatility. This seems sensible to me, after all a 10% rally from here and the central bank would end up looking a bit reactive and silly. We’ll get a better sense about exactly what they’re thinking in today’s ECB press conference. Across the world in Japan, similar questions are being asked of the Bank of Japan, the currency has appreciated significantly against both the renminbi and dollar in recent months, and on top of that the Nikkei has dropped 20% from its summer peak. I wonder if the BoJ will do anything, given the fact that Japan is a huge commodities importer, they are surely benefitting from the current weakness, and the reality is that short of risking hyperinflation they are doing a lot already to boost inflation. I suspect the answer will be dependent on how much the Japanese yen continues to appreciate.

The falling oil price continues to devastate oil producers, it isn’t an exaggeration to say that the Russian rouble is in freefall at the moment. The Nigerian naira is also under severe pressure. Here is a representation of the parallel market rate in recent times…

It’s tough to say when this ends, but you can see that the naira is at record lows versus the dollar. There’s no immediate reason to think that it gets better, particularly as crude oil continues to fall.

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc