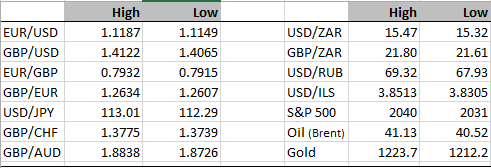

Already this morning the dollar has made new highs for the week versus the euro, Japanese yen and British pound, as clear a sign of trend as you’re likely to get. Whether it’s a re-repricing of potential rate hikes in the United States later this year or supply demand factors, it’s happening, and we have to deal with it. It actually makes sense when you consider the recent comments of Charles Evans an FOMC member and a known dove, “Two rate increases not at all unreasonable”. That’s where the Fed is right now, 2 rate hikes forecast for 2016. So what does it mean when one of the most dovish decision makers is suggesting that that’s the least they should do? I’m guessing it implies that not only are those two hikes a near certainty but they might not actually be enough. As I mentioned in a recent blog, core inflation in the United States has actually been creeping higher, and so it was interesting that the last FOMC statement appeared to disregard any significant inflationary threat. Is it possible that the Federal Reserve might end up behind the curve on inflation this year? That’s probably not as farfetched as it might seem, let’s not forget that the labour market continues to tighten. One could almost feel sorry for them, considering the tough decisions they’ll have to make.

As I write, GBP/USD is within a few pips of breaking the key level I mentioned a few days ago. While I wouldn’t go so far as to say that it confirms the bearish trend, it does greatly increase the probability that we will indeed see new lows for cable in the weeks ahead. But where cable is concerned it’s important to realise that the move is as much to do with sterling weakness as dollar strength. You only have to look at EUR/GBP which continues to power higher. 0.80 doesn’t seem far away at all now, and we could be there even at some time today!

Elsewhere the Nigerian government looks set to approve a huge budget. You would think that collapsed fiscal revenues could spur belt tightening, but the opposite seems to be true. While I agree with one of the rationales, that Nigeria will never rid itself of its dependence on oil without building the infrastructure required to sustain a non-oil economy, I’m not convinced that a coherent plan has been put in place to achieve that objective. Nor do I have any faith in any government anywhere setting the agenda in terms of industrial policy. It is not yet clear to me what these investments the government wants to undertake are, so I’ll withhold judgment until more facts are available. We only need to focus on trying to understand how the excess government expenditure will be paid for. As things stand we are told that there have been discussions with the IMF and World Bank for loans, but the sums in the budget are so large that surely there’ll have to be other sources of funds as well? Watch this space, we’ll report as we find out, it could have a significant effect on the trajectory of the currency which has been doing reasonably well (relatively!) in recent days.

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc