The one key takeaway we get from the much anticipated Chinese GDP data release is “stabilisation”. Q1 2016 GDP came in as expected in China, at 6.7%. Down a smidge on the Q4 2015 number (6.8%), but well within the forecast range of the Chinese government. It seems that rebalancing the economy is taking a backseat for a while as the government struggles to alter what was starting to seem like a dangerous looking downward trend. In the long term however the reliance on construction and heavy industry is simply not sustainable and the government knows it. The plan remains to try to move the Chinese economy towards a more services oriented consumer economy. That is a goal that will take a generation to achieve however.

The IMF have done it, even President Obama has done it, and yesterday the Bank of England did it as well adding its voice to the clamour warning about the risks to the UK’s global standing and the likely negative impact on the economy should Brexit happen. As expected yesterday the MPC was unchanged in its view that rates should remain on hold with all 9 members voting to hold. The Bank believes that fears about Brexit are already dampening economic activity in the UK. This has not pleased those in charge of the ‘Leave’ campaign who claim that the Banks intervention was political. This is patently false as the UK central bank has a duty to discuss any issues which are likely to impact the British economy. It seems like inflation is not even a part of the discussion at the MPC seeing as at the margin prices look to be picking up in the UK. We are seeing a similar phenomenon in the Eurozone based on recently published data, while funnily enough, in the US, the economy most likely to raise rates inflation has slipped back.

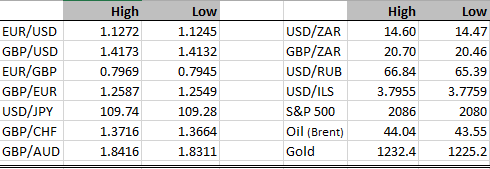

Meanwhile sterling has remained under pressure versus the US dollar. Truth to tell most currencies have been under pressure against the dollar this week. Sterling has actually held its own against the euro in recent days, as the euro has fallen more quickly against the dollar. I suspect this should be looked at as more of a counter-trend move for EUR/GBP. We continue to expect sterling weakness in the face of Brexit.

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc