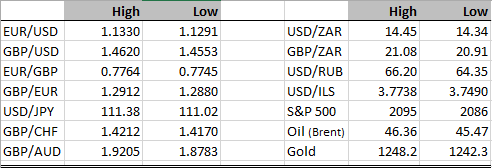

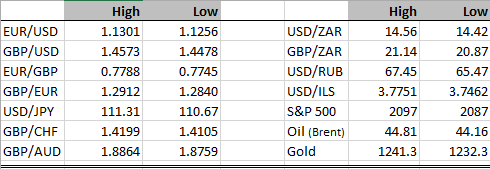

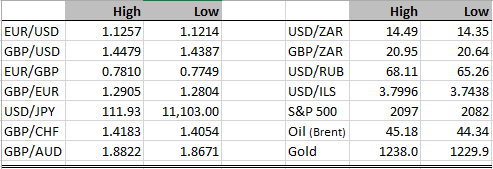

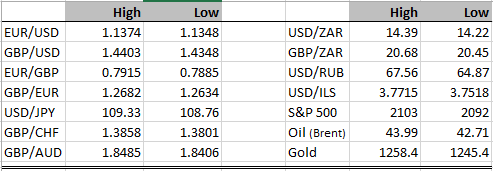

Two major central banks have made their decisions over the last 24 hours, the US Federal Reserve and the Bank of Japan. One was roughly as expected, the other, perhaps not so much. I should add that there were other central banks – New Zealand and Brazil – who also made decisions, but of course those have to be considered less impactful on the global economy. They all left rates unchanged, albeit the rationales for their decisions varied.

FOMC – The statement showed that policy makers are less concerned about the global economy and systemic risk than in their previous meeting. This is not that surprising given the rally in stocks since the last meeting (see the chart of the S&P since the March 15-16 meeting).

However they noted that recent data has shown a domestic economy in which growth has slowed a little and household spending has been lacklustre. There wasn’t any new statement elaborating on the balance of risks, whether external hazards or domestic positives, which might have shed some more light on their future decision making. It’s fair to say that the FOMC has left room to raise rates at future meetings, even June, but we would all be wise to keep a close eye on activity and inflation data between now and then. Another issue to be mindful of is the fact that the UK’s EU referendum will be close to the next scheduled FOMC meeting. If the outcome is uncertain it’s likely to influence Fed thinking in my view, Brexit could be a disaster for markets. In the immediate aftermath of the announcement dollar traded in the same range as it had before, but this morning it has weakened, which leads me on to the other major central bank announcement.

Bank of Japan – the rally in USD/JPY over the last few days in anticipation of the BoJ meeting was as a clear a sign as any that the market was expecting and even hoping for more stimulus in the face of an economy slipping back into deflation. We didn’t get it! Perhaps it might be too soon to call the whole Abenomics strategy into question, but some recent trends have been a blow to Prime Minister Abe’s growth programme. The BoJ looks to be relying on the recovering US economy, a stabilising Chinese economy boosting Japanese business confidence, he’s also betting that a stronger yen shouldn’t be as damaging for Japanese businesses as it might have been in the past. I have a lot of sympathy for the latter view, Japanese corporates have spent the last decade moving a huge chunk of their operations offshore, I’ve always suspected that the positive benefits of a stronger yen are at least a match for the negatives now. The only issue might be the negative impact of translation effects on earnings, and thus the Japanese stock markets. Anyway, the point is that the yen surged in the wake of the BoJ lack of action and other major currencies have gained ground on the dollar as well, although not to the same extent as the yen.

In terms of the bigger picture, I still look at the dollar as being in a corrective pattern, there’s ample room for more weakening, but the next major move in my view will see the greenback strengthen. It could be some time before that happens…

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc