It’s really starting to look like the next leg down in sterling is beginning. As I said in a recent blog, I’m loathe to call it until we make a new low. Elliotician’s (practitioners of Elliott Wave Theory) will know what I mean by this… it’s always difficult to differentiate between a ‘B’ wave and the start of a new impulse wave until you get reasonable clearance from the previous low. Not only is sterling weakening but the euro is as well, which is what I expected for the next leg down, don’t get me wrong, sterling is underperforming the euro at the moment, but it’s not looking good.

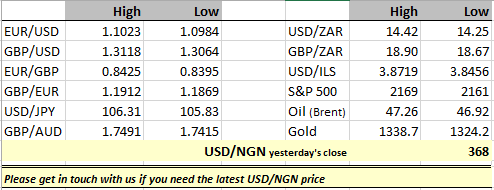

GBP/USD…

EUR/USD….

Why should this be happening now? Well… Prime Minister May has made a political calculation which is feeding market uncertainty. It’s either genius on her part, or a horrible mistake. The political calculation I’m making reference to is her decision to stall on pushing ahead with Article 50 which will trigger the exit of the United Kingdom from the European Union. I mentioned in a recent blog, that following discussions with Nicola Sturgeon, the Scottish First Minister, Prime Minister May has determined that Article 50 will only be triggered with some buy in from Scotland. I can well understand her desire to maintain the integrity of the United Kingdom, but the short term cost is uncertainty. I will never be able to say this often enough… MARKETS HATE UNCERTAINTY. This is what we’re experiencing right now, as businesses come to terms with a lack of clarity regarding the United Kingdom’s relationship with the European Union. What we’re seeing at the moment are stock markets trying to hold on to recent gains, but I have to say, European bourses in particular (not including the UK markets) do not look great. The recovery since Brexit was announced has seen some bourses around the world make new highs – particularly the FTSE 100 and S&P 500 – but not Continental European stock markets. The recovery we have seen for Continental markets have been distinctly corrective. If they turn, and turn hard, I suspect they’ll take global markets with them.

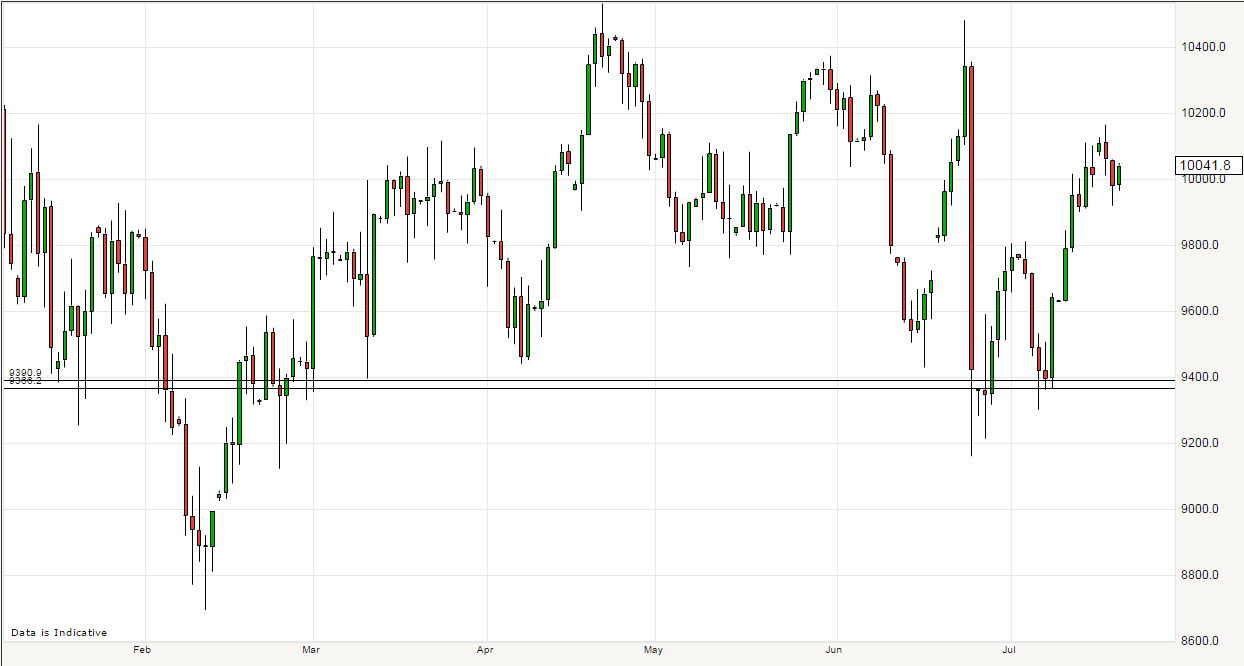

FTSE 100…

DAX…

Economists – the “experts” that the former UK Minister Gove dismissed, are increasingly pessimistic about the outlook in the UK, and consequentially the Eurozone. Investment is likely to take a big hit while the uncertainty persists, and there’s no reason to believe, given Prime Minister May’s decision that this state of affairs will change this year. Indeed the IMF has just cut 1% point of UK growth forecasts for 2017, and that’s not their worst case scenario! A former MPC member was on tv last night suggesting that the Bank of England should act decisively to add liquidity to the UK economy. If they get it wrong what’s the worst that could happen, higher growth and asset prices, but to get it wrong could lead to a significant fall in output. What does he think we have to fear? Falling business investment as long as uncertainty persists, falling house prices too (already reports are coming out showing sales of new London homes are at a 3 year low). Let me just add, if some of the doom sayers are right and house prices do fall, this could set off a feedback loop into consumption in the UK that will be hard to correct. In that scenario it is clear that the Bank of England will be forced into an aggressive programme of quantitative easing

You don’t have to be a genius to figure out what the implications for the currency markets are. If the Bank of England does nothing, or doesn’t respond quickly enough, we could see confidence and investment fall, leading to further significant declines in sterling, and I believe the euro will also be affected albeit to a lesser extent. If the Bank of England does act, then sterling will still fall. Quantitative easing tends to do that to currencies, but perhaps the euro will be less negatively impacted. Either way, this all looks very very bad for the pound. We might look back at GBP/USD trading at the 1.30 levels with some fondness in a few month’s time. This does not look good at all!

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc; and at www.parityfx.com