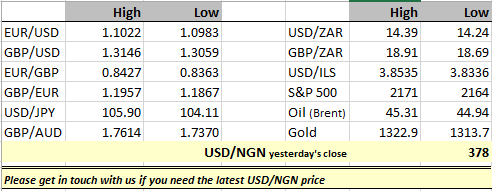

When Natwest, one of the main UK High Street banks issues a notice to its corporate customers that there is the possibility of the bank applying negative interest rates to their deposits you can almost take it as a certainty that rates are going lower in the very near future. Most expect the Bank of England to announce a rate cut in August, and this is as clear an indication of that as you can get. The situation becomes even clearer when you hear the likes of Martin Weal, a member of the Bank of England’s monetary policy committee, having seen the negative business surveys published after the referendum stating that he now thinks immediate stimulus to the UK economy is necessary. We may have not seen the last of sterling weakness, brace yourselves.

Trading volumes have risen as the S&P has made new highs, this is normally a good signal that the trend is likely to be persistent and a genuine breakout has occurred. The post global financial dynamic of markets reacting positively to anticipated stimulus continues. As things stand it’s likely we’ll see stimulus from both the UK and Eurozone central banks. In a way it’s odd to see oil quietly retreating from the highs as has been the case in recent weeks, but perhaps the snippet I put into a recent blog – the US is now exporting gas to the Middle East – is a more powerful indicator of the state of play than the effects of more stimulus.

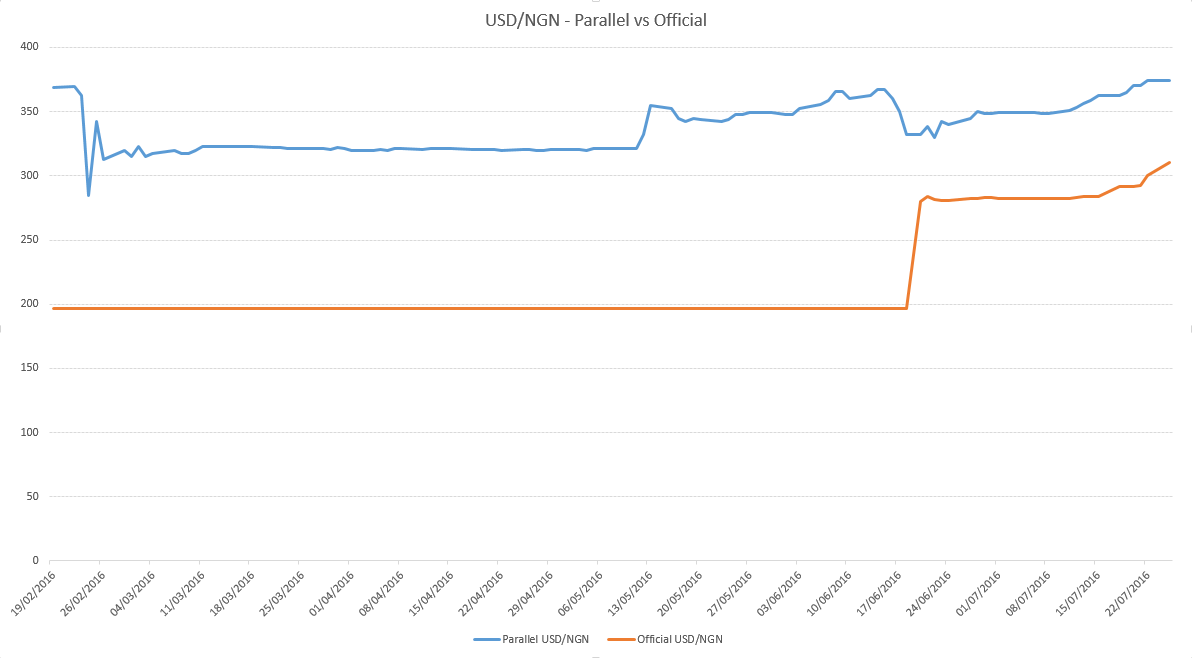

Elsewhere it’s clear that the Nigerian central bank has managed to bungle what seemed like a sensible devaluation plan. On reflection, an effective freeing of the naira should have led to a more rapid convergence of parallel and official market rates than we have seen so far. Certainly, with supply and demand reaching a balance of some sort, we would not be observing (and experiencing) such a severe shortage of dollars as is currently the case.

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc; and at www.parityfx.com