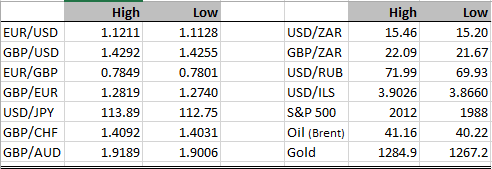

He didn’t cry wolf this time he acted, but by the end of ECB President Draghi’s press conference the euro was flying. The ECB announced a larger than anticipated plan to expand quantitative easing, incentivised banks to increase lending (good luck with that one) and pushed rates further into negative territory. Given that one of his objectives was surely to weaken the currency this wasn’t much of a success. I’ll come back to that later, but it’s fairly obvious when he lost control of weakening the euro (my assumption of his strategy was that a weaker euro was one of the aims). This was when he indicated that the central bank was uncomfortable with going deeper into negative rate territory, for fear of damaging banks. By the way you don’t hear him worrying about damaging an increasing number of pensioners who rely on fixed income! As soon as he made this comment effectively casting doubt on further rate cuts, the euro – which had dropped on the announcement of more QE and rate cuts – reversed sharply. Check out the chart of EUR/USD below, the vertical line is the time of the announcement of the cut and more QE. No prizes for guessing when he cast doubts on further moves deeper into negative territory! The bottom line is that the market now believes that currency depreciation is no longer considered a viable strategy by the ECB. Not surprisingly a large proportion of the short EUR/USD bets in the market place were reduced. Does this mean that all of a sudden we should be bullish on the euro? Absolutely not. The conditions are perfect to borrow in euros (if rates are negative you should actually get paid for your troubles, at least in theory) in other words sell euros, and invest in higher yielding assets. It might take a while for this dynamic to gain traction as there are many countervailing forces out there, not least short term trading noise.

Despite the less than stellar performance of the euro, equities are perhaps reacting a little bit more positively to the ECB’s actions. That’s not to say that there wasn’t an adverse reaction to Draghi’s revelation about discomfort with deeper moves into negative rate territory. Certainly after the initial rally, equities also fell and made new lows for the day, but today they are up again. The reality of more quantitative easing will be good for equities, as will the fact that alternatives to further rate cuts are likely to be directly beneficial to risky assets. So this seems like a logical reaction. It is hard to say if this is what Draghi intended, but personally I would err on the side of giving him the benefit of the doubt. After all, this is the man who early in his term, came out strongly and said that the central bank would do “whatever it takes” to save the single currency. The fact that he was so bold and blunt, ensured he didn’t really have to do much more. For someone astute enough to understand market perceptions at that time, it’s hard to believe he wouldn’t appreciate the consequences of casting doubt on deeper moves into negative rate territory now. I’ll have to sit down for a while and figure out what game he might be playing, I can only admit that it isn’t totally clear to me at the moment.

In other news, I note with interest quite a noticeable drop in initial jobless claims in the US. It’s only one month’s data, further data points are needed before we can make something of it. If it’s the start of a new acceleration of jobs growth in the United States, we might have further reason to remain longer term bearish EUR/USD.

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc