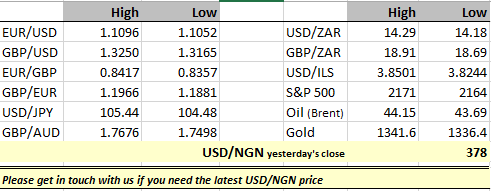

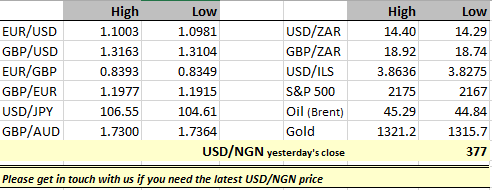

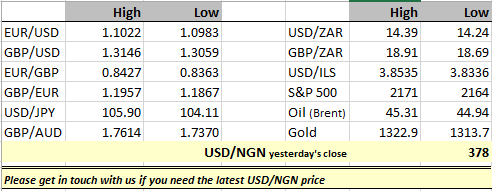

| High | Low | High | Low | |||

| EUR/USD | 1.1338 | 1.1270 | USD/ZAR | 13.65 | 13.41 | |

| GBP/USD | 1.3157 | 1.3031 | GBP/ZAR | 17.88 | 17.51 | |

| EUR/GBP | 0.8683 | 0.8608 | USD/ILS | 3.7935 | 3.7391 | |

| GBP/EUR | 1.1617 | 1.1517 | S&P 500 | 2186 | 2175 | |

| USD/JPY | 1,009.95 | 100.19 | Oil (Brent) | 51.08 | 49.40 | |

| GBP/AUD | 1.7243 | 1.7106 | Gold | 1342.0 | 1331.0 | |

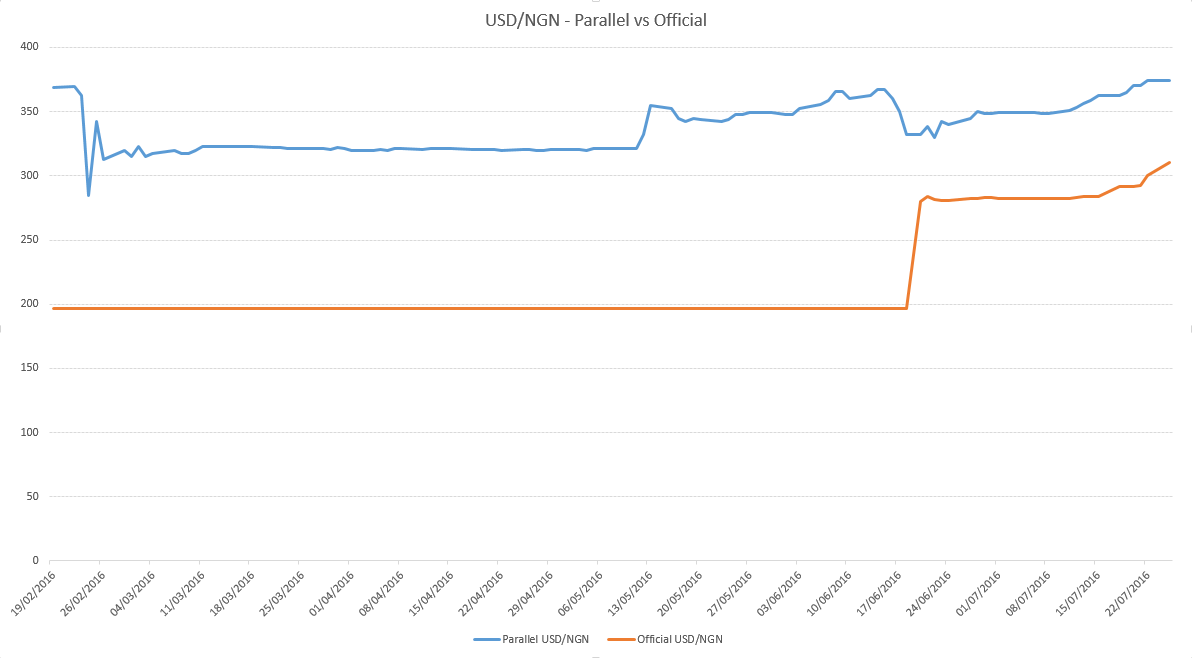

| USD/NGN yesterday’s close | 395 | |||||

| Please get in touch with us if you need the latest USD/NGN price | ||||||

After the yo yo effect last week following the inconclusive FED minutes, we started the week on a USD down day. I am not too surprised to be honest as I have been saying if the FED stick to what they have told us they will delay hiking rates. But what they tell us and what they do are quite simply 2 very different beasts. You see Pres. Yellen and her board members are obviously not in agreement about US rates and whether they should in fact be hiked in September. Personally if I was a board member I would vote to hold for now especially with the Nov US elections just around the corner. We should hopefully get a little more colour later in the week when Pres. Yellen speaks at Jackson Hole (to global Central Bankers). While I am sure she will dangle the carrot I doubt it will be edible. In other words, she will keep her cards close to her chest and let us keep guessing whether or not they hike or not. The data in the US has been ok and shows continued signs of an economy that’s in ok shape, however the same cannot be said for the EU/China and the UK. In fact the global economy is now facing a situation where the former is outpacing the latter group and that is no fun at all. It is for this reason I think we will next see a rate hike in December as intimated earlier this year. There is no rush. But having said that and having mixed with Central Bankers I kinda see why and how they would vote to hike rates in September. After all how much “damage” could a 0.25% hike really have….erm, lots!!! But they know that. So while the FED are split I think Pres. Yellens casting vote could in fact swing it her way (hike) and then sit back and see how the domino’s fall.

What this all means is if we do see a rate hike the USD will move like a bullet train on the back of asset allocation as traders and financiers move their assets heavily in favour of the USD. The hike would be a real boost signalling things are ok and the global economy can withstand and absorb a 0.25% rate hike. As far as the GBP is concerned, if you shut your eyes and sold the GBP when you walked in this morning and then opened them and decided to “take profit” I am afraid to say there would be none. The GBP dropped 60pips through the day and is back to trade around the opening levels. Seems Europe likes to sell the GBP and the US likes to buy it. Unless something silly happens over the coming days, all eyes will be on Friday and Pres. Yellens speech. So I think for this week the GBP will drive in a range between 1.3000 – 1.3200 awaiting further news on Brexit and Yellen.

Talking about Brexit, I mentioned Friday that negotiations will commence in 2017 (July onwards) and I guess someone in Whitehall must have read my blog because we now know that there is a big chance of that in fact happening. A year to get their ducks in a row and a year to prepare for “war”. The EU are unlikely to cede to the UK’s desires on trade and migration. The UK will try to muscle their way through the negotiations but if the Canada/EU negotiations are anything to go by I think this will be a game of chess. I wonder who will blink first.

Financiers businesses individuals and traders are all coming to terms with the new GBP rate. Before I go let me throw this at you. All the reports I am reading these days are saying that the catastrophe that will ensue if the UK voted OUT are actually not as bad as it appears. Stocks are at near year highs, businesses have not reported a collapse in trade and have simply passed on higher costs to the consumer who is happy to pay regardless. Inflation has ticked up as a result of increasing prices (to the satisfaction of the BoE). Granted the UK’s GDP is not into the 2% mark we have been accustomed to, but hey even at 0.60-0.8% I guess we can live with that. SO my question, if things are not as bad as they appear why can’t the GBP rally say back to 1.3500-1.38-1.4000 until the negotiations actually start. DO you see where I am going with this!! Funnier things have happened. Be prepared for the unexpected.

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc; and at www.parityfx.com