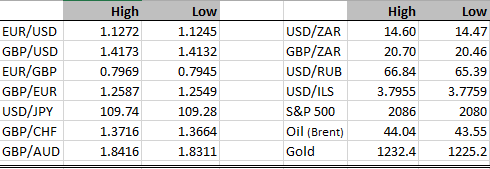

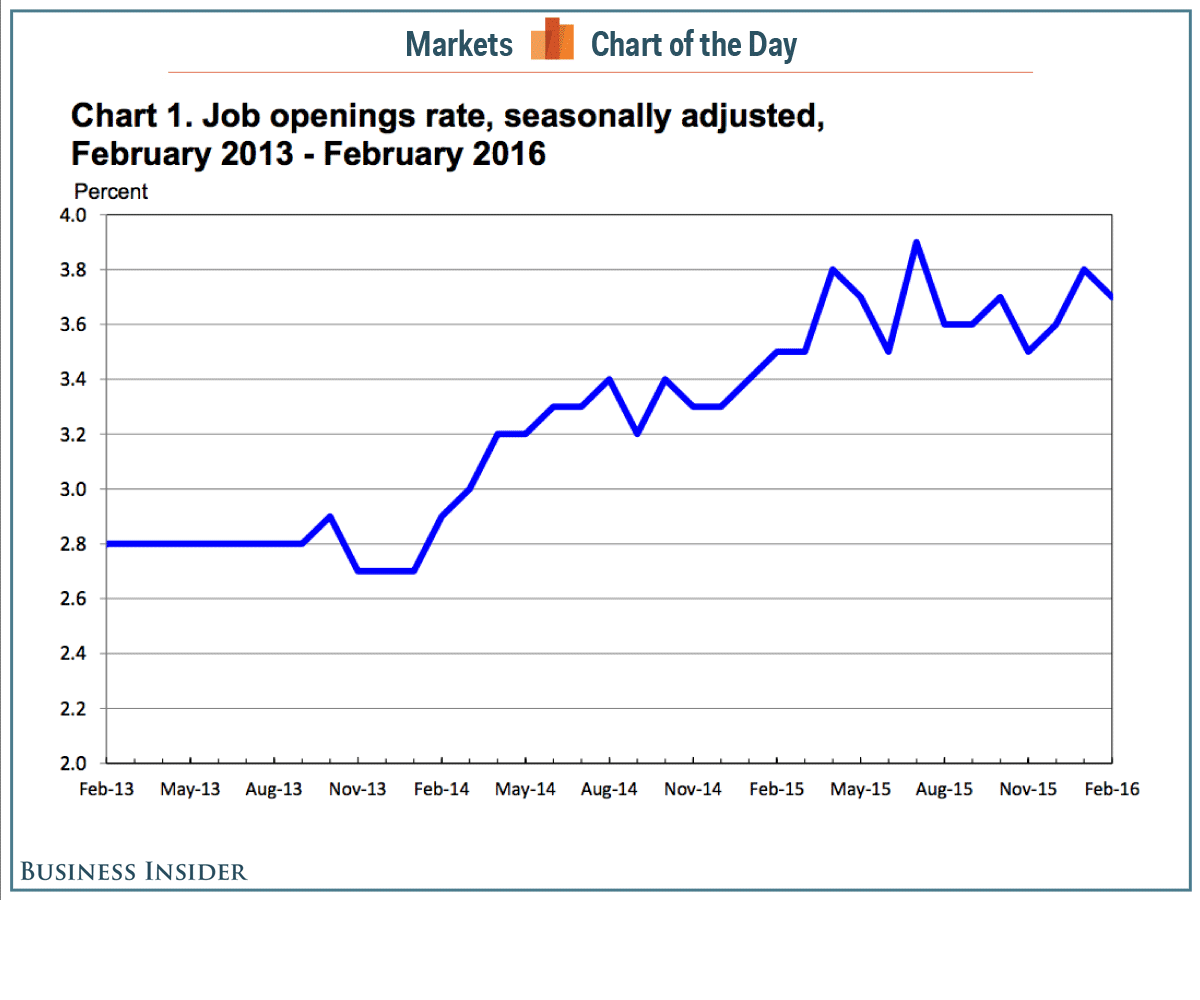

Risk sentiment continues to improve with S&P 500 now trading above the key 2100 level. The next target is the early December reaction high at 2116, which is also the level of the downward sloping resistance trend line demarking the lower highs since the ultimate peak last summer. It’s hard to imagine that record highs aren’t in front of us in the coming months.

Quite a turn around since panic at the start of the year, and a complete contrast to the doom and gloom mongers at institutions like the IMF. Why would equities be climbing like this if the global recovery is stuttering? If the global recovery is still intact then at some point a reassessment of the Fed outlook and the hiking cycle in the United States is inevitable and it’s interesting that Rosengren, seen as one of the most dovish voters at the FOMC, has opined that the market could be underestimating the health of the US economy. And therefore the likely path of interest rates. I quote.. “The very shallow path of rate increases implied by financial futures-market pricing would likely result in an overheating that necessitates the Fed eventually raising interest rates more quickly than is desirable, which could endanger the ongoing recovery and continued growth” (Bloomberg).

Elsewhere there are signs that the macro news is getting better, at least in the short term. I was stunned to read, in the Financial Times, that house prices in leading cities are up 63% year to date, albeit they are falling in smaller cities. This should give a boost to activity in these major cities that will be of benefit to the Chinese economy in the short term. Although it feels like it’s just storing up more problems in the longer run. Perhaps we can hope that in the long term other economic regions around the globe pick up the slack and permit China to continue it’s much needed economic restructuring.

The dollar looks a bit weak in early trading today, but I can’t help feeling that the more positive the economic news we get, the more likely expectations of a more hawkish Federal Reserve will start to boost the dollar.

DISCLAIMER

Any financial promotion contained herein has been issued and approved by ParityFX Plc (“ParityFX”); a firm authorised and regulated by the Financial Conduct Authority (“FCA”) as a Payment Services Institution with registration number 606416. It is for informational purposes and is not an official confirmation of terms. It is not guaranteed as to accuracy, nor is it a complete statement of the financial products or markets referred to.

Opinions expressed are subject to change without notice and may differ or be contrary to the opinions or recommendations of ParityFX. Unless stated specifically otherwise, this is not a recommendation, offer or solicitation to buy or sell and any prices or quotations contained herein are indicative only. To the extent permitted by law, ParityFX does not accept any liability arising from the use of this communication.

Follow our tweets @parityfxplc

Follow us on LinkedIn ParityFX Plc